多元回归分析代写 Lecture 1: Multivariate Regression Analysis

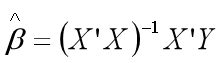

多元回归分析代写 Under these assumptions we have the ordinary least square (OLS) estimator:The matrix

is often referred to as the projection matrix…

Unknown parameters:![]()

Assumptions:

(Note

(Note  is constant)

is constant)

Under these assumptions we have the ordinary least square (OLS) estimator:

The matrix ![]()

![]() is often referred to as the projection matrix

is often referred to as the projection matrix ![]()

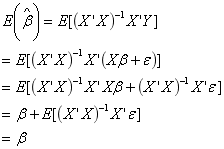

Sampling properties of the OLS estimator:

- we look at the property of unbiasedness for

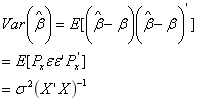

- The variance-covariance matrix for

is given by

is given by

![]()

Given the unbiased property, the next question concerns comparison with other linear unbiased estimator. The Gauss-Markov theorem states:

![]()

Thus, ![]() BLUE

BLUE

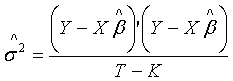

Having obtained a point estimator for the unknown parameter![]() , we now turn to estimating

, we now turn to estimating![]()

Where T is the number of observations and K is the number of explanatory variables.

![]() is an unbiased estimator for

is an unbiased estimator for![]()

t-value=![]()

Summary: 多元回归分析代写

- First, calculate

- Second, using the estimated

, calculate

, calculate

- Third, generate t values for each parameter

- Finally, analysis your results.